- About

- Topics

- Story

- Magazine

- In-Depth

- Opinion

- News

- Donate

- Signup for our newsletterOur Editors' Best PicksSend

Read, Debate: Engage.

"We could not get out of the climate agreement even if we wanted to," said John Kerry, then US Secretary of State, to the crowded press tent in Marrakech, the Moroccan city, where steps to implement the Paris Climate Treaty were negotiated in November 2016. His speech was addressed to Donald Trump, who had been elected to the designated US president the week before. "To try that would not be a political failure, but a moral one."

"Not politics, but markets dictate climate protection," Kerry said in Marrakech. The baton now has to go from politics to the economy.

Capitalism as a sheet anchor of the Climate Movement? It sounds grotesque.

The fact that the new leader of the United States of America would be unimpressed by such reminders must have been clear to most of the audience in the room. And indeed, just a few months after his inauguration, Trump announced the withdrawal from the Paris Agreement.

Kerry also saw this step coming. In his speech, he appealed not only to reason, he also conjured up forces, which Trump seems to feel much more familiar.

But is it?

On the negotiating floor in Paris, the world has agreed to limit the global temperature rise to well below 2 degrees Celsius. In order to achieve this goal, the states have committed themselves to setting their own climate goals and reviewing them on a regular basis. The Paris Agreement thus implements the G7 decision of Elmau, which calls for a complete decarbonisation of the world economy. Not only the fossil energy sector is affected, but all sectors. Industry, transport, agriculture.

Therefore, in the French capital not only tougher climate goals were decided.

The signing of the contract leads to a conversion of the entire financial architecture.

Article 2.1 of the framework is set to do so. It states that all capital flows should be brought into line with a development path free of carbon dioxide.

As a result, the Paris Agreement sends an important signal to investors. Companies that continue to produce emissions intensively could soon turn out to be no longer lucrative.

The British economist Nicholas Stern speaks of "technological cost traps", and at the same time recommends investors to convert existing investment plans at an early stage. The Paris Agreement is already a milestone in climate diplomacy. Countless attempts were made to negotiate a contract that almost all the countries of the world feel committed to. A new feature of the treaty is that, while taking all responsibility into account, the States still have sufficient scope for implementation.

Another new feature is that not only the many governmental delegations have contributed to its success, but also the countless helpers on the side line. Scientists, climate activists, company bosses. For the first time, they did not face each other in opposing parties.

Paris became a place where a narrow, though pragmatic, act of solidarity of different forces could be observed. Not an unfortunate alliance, rather a community of interests, considering respective advantages. Pareto optimal. Not united by ideology, but probably by the common concern. An alliance of climate protectors and investors.

For the economy, the unabated rise in temperature is bad for business. When weather catastrophes throw a spanner in the works of global trade chains and lead to reductions in revenue. Not surprisingly, climate protection has become the new entry in manager's glossary. Risk management instead of mere company responsibility.

And climate change poses many risks. Especially when agreed climate goals have the scent of regulation and some companies are already in court. Exxon Mobil for not passing on internal climate knowledge to the public. RWE for its emissions causing damage elsewhere.

All this played an important role in Paris. Already months before the start of the negotiations, the French finance minister had asked the G20 group to investigate how climate change could affect international financial stability. A little later, the Financial Stability Board started its work, launched already in 2007 in response to the world financial crisis.

Mark Carney, head of the agency, had previously attracted great attention with his own report. He laid out why the British insurance industry is already affected by the global temperature rise. Therefore, Carney, who is also governor of the Bank of England, has been seen as something like the figurehead of smart climate protection.

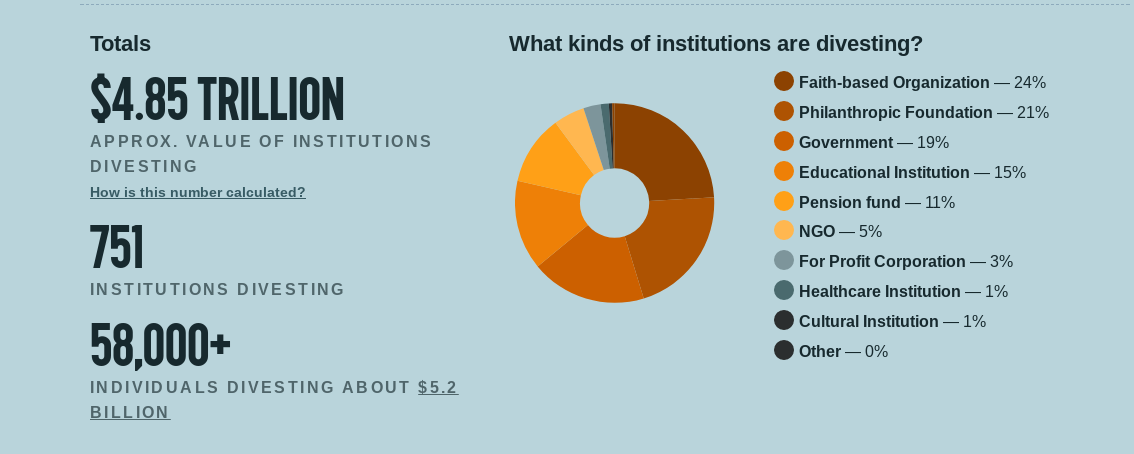

This is especially true for the climate protection alliance "Fossil Free". The initiative wants climate-damaging businesses to be closed down and calls investors for "divestment", ie selling shares of companies in fossil fuel industries, ie coal, oil and gas.

With its demand, the movement has been making big headlines for years now, especially in the USA. Climate protection by means of boycott, that appeals to many.

Divestment is free of any ideology.

Divestment is not apolitical, but also not anti-capitalist.

Divestment is not directed against the government or the economy, but is instrumentalizing both.

Divestment is social necessity and economic self-interest at the same time.

Already in 2015 analysts of the Citi Group, one of the major US-American banks, warned of a possible financial bubble ("carbon bubble"). The reason: if a large part of the fossile fuels were burnt, the climate goals would be impossible to achieve. If they were to be respected, however, energy companies would be stuck with their fossil reserves and would thus become a risk for investors, as they would have to fear a sudden loss of value of their investments.

Not only climate change, but also the fight against it could put companies and investors at unimagined risks. A classic dilemma. In many countries, debates are aroused as to how the financial world can once again master the situation. Some governments have therefore already imposed stricter reporting requirements.

France, for example. Since the beginning of the year, investors have to disclose how they want to deal with climate risks in their portfolios.

More information, they assume, would help to forecast the extent of the imminent losses. Even some central banks are now thinking about climate stress tests.

But another trend is also emerging. Instead of political intervention, corporate self-commitment is increasingly relevant. The message: The economy will fix it.

From main street to Wall Street,

new initiatives are emerging which are trying to anticipate regulatory measures and to develop their own plans to take climate change to open up promising new markets.

Because where risks are lurking, there are also opportunities.

Renewable energies, for example. According to the Climate Policy Initiative, in 2014 alone, about 392 billion US dollars were spent on climate protection initiatives - more than ever before. The majority comes from private investors. In many parts of the world, the increase in investment makes renewable energies competitive and thus produce electricity cheaper than fossil fuels.

This is putting pressure on operators of classic industrial plants. In China and the USA, the world's largest issuers of hazardous greenhouse gases, many coal-fired power plants had to close down already. Similarly, the tar sands industry in Canada is coming to a standstill because of the shale gas boom in the USA. The market is turning and with it the investment appetite of large investors.

And politics react. In order to meet climate goals, a tight political framework has now been set up, with suggestions of G7, G20, EU and UN working groups currently underway, providing all kinds of guidelines and criteria for a sustainable financial regulation.

But all that glitters is not - green. While the divestment movement can report almost new successes every single day, it is by no means clear whether and to what extent the supposedly freed up money flows into sustainable alternatives. And what is sustainable anyway? The concept of sustainability has been overstated by its inflationary use to the point of being unrecognizable, and has become a formula for just about everything: often for the well-meant, rarely for the well-made.

Therefore: divestment is necessary, but not sufficient. For with the sole withdrawal of capital, the climate will still need more efforts of protection. The International Energy Agency assumes that funds of around US $ 16.5 trillion will be needed to comply with the Paris Agreement. In addition, the divestment movement is at risk of becoming a game of public relations strategists: when divestment decisions make headlines without any measureable effect.

Nevertheless, the divestment movement is promising. It shows the shady side of an overhauled industry and, by means of catchy formulas, can translate the otherwise complex climate science into a simple pictorial language and make it mass-efficient. This is perhaps a parallel to the government style of Donald Trump. With a difference: reason and facts form the core of this new movement.